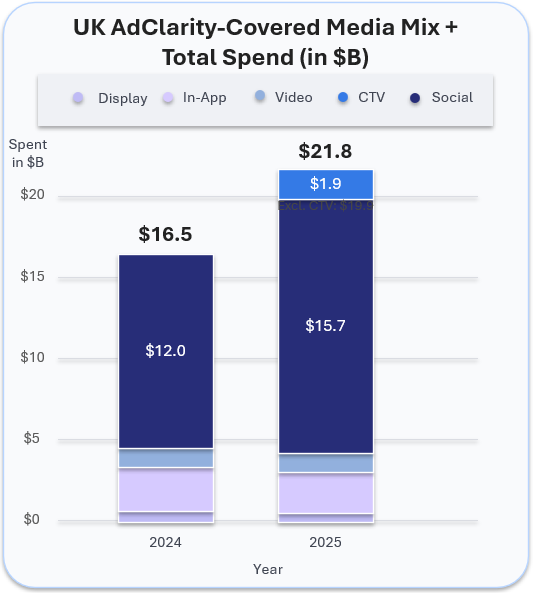

Looking at last year’s advertising data, the UK digital ad market delivered strong growth in 2025, but the headline number comes with an important qualifier. Based on AdClarity by BIScience tracked market data, total measured spend across Social, Display, Video, CTV, and In-App ads reached approximately $21.8B in 2025, excluding search and retail advertising.

Because CTV was tracked by AdClarity in the UK only from 2025, that total is not directly comparable year over year on a like-for-like basis. On a comparable basis excluding CTV, tracked UK spend rose from about $16.5B in 2024 to about $19.9B in 2025, representing 20.6% growth. That still points to a very strong year, while giving a more accurate apples-to-apples view of how the market expanded.

What stands out even more than the growth itself is the shape of the mix. The UK remains heavily concentrated in Social, while other channels play much smaller roles. At the same time, 2025 marks the first year in this dataset with measurable CTV activity in the UK, adding an important new layer to how brands distribute budgets.

Social Still Sets the Pace

Social remained the clear center of gravity in the UK in 2025. Spend rose from about $12B in 2024 to $15.7B in 2025, a gain of just over 30%, while Social held roughly 71.8% of total tracked spend. In other words, nearly three quarters of the measured market still flowed into Social.

That level of concentration is far higher than in the US, where Social accounted for about $83.3B in 2025, or just under half of tracked digital spend. The contrast suggests that UK advertisers still rely much more heavily on Social as the default engine for reach, scale, and ongoing optimization, while the US market is spread more broadly across channels.

CTV Arrives While Other Channels Stay Tight

The biggest structural shift in the UK data is the arrival of CTV. There were no tracked UK CTV channels in the 2024 dataset, but in 2025 CTV accounted for about $1.9B in spend. That means CTV should be read as a new layer added to the market in 2025, rather than as part of a direct year-over-year comparison.

Outside that change, the rest of the market was more restrained. Video was broadly flat, Display declined, and In-App also moved down year over year. Social remained the dominant tracked channel, but the addition of CTV makes the 2025 media mix more diverse than it appears in a like-for-like comparison alone.

What the UK Market Is Telling Us

Taken together, the 2025 figures point to a UK market that is growing quickly but not evenly. Social remains dominant, CTV has entered the picture, and legacy digital formats such as Display are under pressure. In-App is still material, but it is no longer gaining share.

That pattern matters for competitive planning. In a market this concentrated, even small shifts in channel allocation can signal a real strategic change. If more advertisers begin to scale CTV while maintaining heavy Social investment, the UK market could start to look more like the US in structure, though not yet in balance.

What Marketers Should Watch Next

For UK marketers, the next question is whether 2025 was the start of a broader rebalancing or simply a year of Social-led expansion with one new channel added to the mix. The smart move now is to watch not only how much competitors spend, but where that spend begins to migrate. If CTV keeps growing and Social remains dominant, the most important competitive story in the UK may not be channel replacement, but channel layering: using Social for scale, CTV for premium reach, and a smaller supporting mix across Video, In-App, and Display.